The high inflation rate is posing significant challenges to Nigerians, particularly the vulnerable and the poor, making it increasingly difficult for people to afford basic necessities such as food, housing, and healthcare. Cowry Research maintains the view that inflationary pressures will persist in the coming months due to adverse weather conditions and the lingering effects of crop diseases, which are likely to dampen the potential benefits of the green harvest. As such, we project inflation to reach 27.10% in September 2023

EQUITIES MARKET: Weak Market Momentum Drags the ASI by 0.11% w/w Due to Sell-offs….

In the upcoming week, we anticipate a blend of mixed sentiments in the market, with positive momentum counterbalanced by profit-taking activities as we approach another potential peak or a possible fake out. This uncertainty is further fueled by the upcoming half-year earnings reports from Accesscorp while investors are likely to continue in portfolio reshuffling in preparation for the quarter-end reporting season. Meanwhile, we continue to advise investors on taking positions in stocks with sound fundamentals.

FOREX MARKET: Speculative Activities Drive Naira to a Historic Low of N998/$1; CBN Sells FX to Banks …..

In the coming week, Cowry Research anticipate the naira to trade in a relatively positive band to show further appreciation at the various fx markets barring any distortions while the apex bank maintains its interventions to shore up the naira value.

MONEY MARKET: Money Market Rates Crash on Ease in Financial System Liquidity…

We expect activity in the money market to be bearish as we expect the CBN to rollover a total N177.12 billion maturing treasury bills across the 91-day, 182-day and 364-day tenors at the next primary market auction….

BOND MARKET: Positive Weekly Outing for the FGN Eurobonds…

In the new week, we expect local OTC bond prices to trade muted as the market seek for trigger for the bullish sentiment in the midst of an expected strain in financial system liquidity…

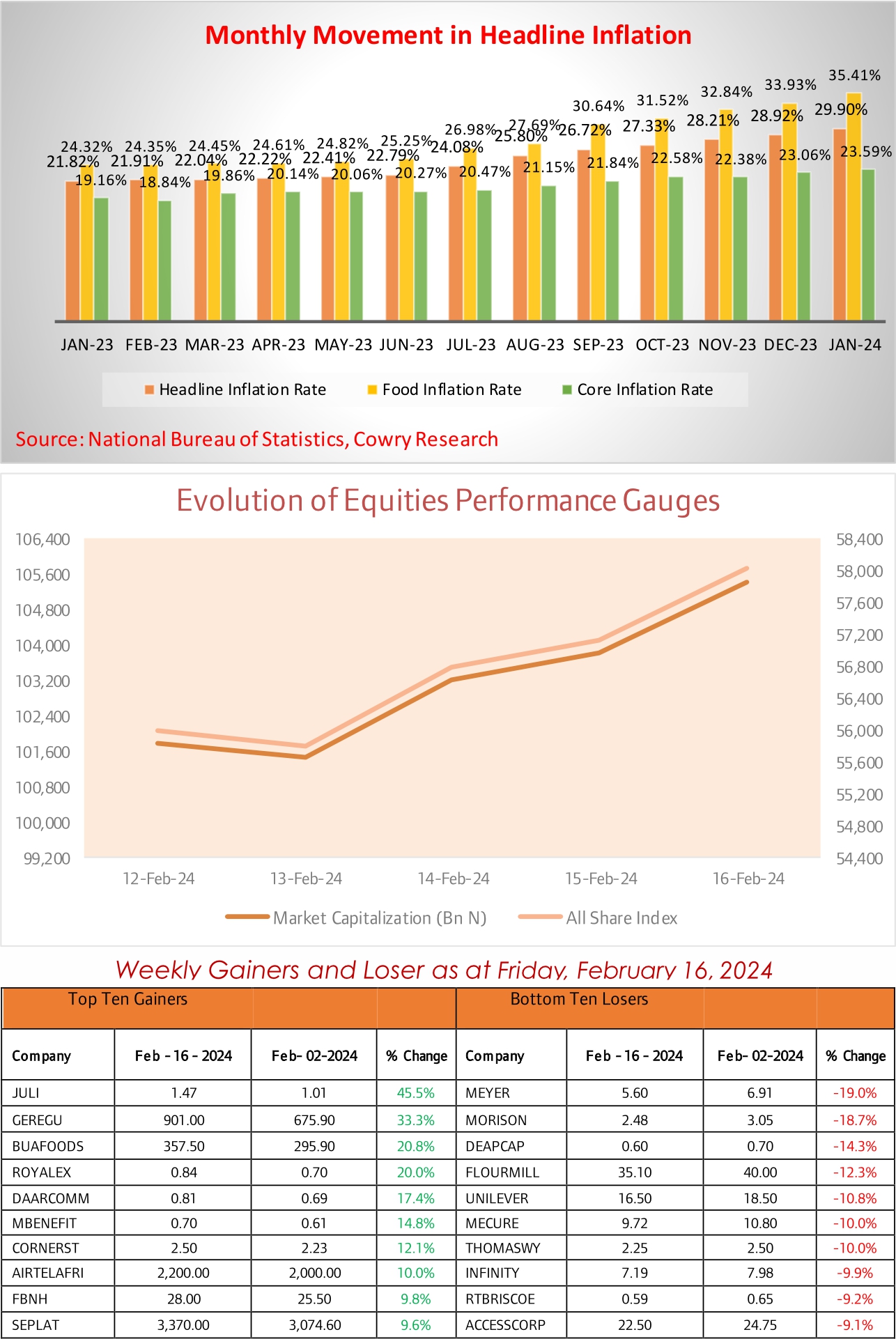

ECONOMY: Unabating Uptrend in Headline Inflation Reading to 25.80% in August….

According to data from the National Bureau of Statistics (NBS), Nigeria’s headline inflation continues to exhibit an upward trajectory in the monthly readings, reaching 25.80% year-on-year in August 2023. This marks a notable increase from the 24.08% reported in the previous month of July and a significant jump from the 20.52% recorded in August 2022. Importantly, this development aligns with our earlier expectations of a surge in inflation for August, projected at 25.50%, making it the highest inflation rate observed in Nigeria since August 2005. Furthermore, it extends the streak of consecutive monthly increases in 2023 to eight months.

The accelerated growth in the headline inflation rate can be attributed to several key factors. Firstly, the downward adjustment of the naira exchange rate is contributing to the inflationary pressure. Secondly, the surge in the price of premium motor spirit (petrol) has been a persistent factor affecting the economy and consumers’ pockets, persisting for two months following adjustments made by the current administration. Additional factors likely driving elevated annual inflation levels include disruptions in the supply of food products, increased import costs due to currency depreciation, rising production costs, and the relatively higher cost of transportation resulting from fuel price adjustments following subsidy removal and the upward trajectory of oil prices. Notably, Kogi (31.50%), Lagos (29.17%), and Rivers (29.06%) reported the highest inflation rates, while Sokoto (20.91%), Borno (21.77%), and Nasarawa (22.25%) recorded relatively slower increases.

Delving into the components contributing to the elevated headline inflation, the cost of food and non-alcoholic beverages stands out as a significant driver, accounting for 13.36% of the divisional-level contributions. Following closely is the cost of transportation, which experienced a 1.68% rise, and the cost of housing, water, electricity, gas, and other fuels, with a 4.32% increase. Other notable contributors include clothing and footwear (1.97%) and household maintenance and furnishings (1.30%) for the month of August 2023.

Furthermore, the food index maintained its upward trajectory, reaching 29.35% year-on-year and marking the highest level observed since September 2005. Food inflation has been on a steady rise since February 2022, with a brief moderation in December 2022. This trend can be attributed to the significant weight of food items in the inflation index. Key drivers of food inflation include increases in the prices of oil and fat, bread and cereals, fish, fruits, meat, vegetables, potatoes, yams, and other tubers, as well as milk, cheese, and eggs. The average annual rate of food inflation for the twelve months ending August 2023 was 25.01%, reflecting a 5.99% point increase from the average rate recorded in August 2022 (19.02%). Kogi (38.84%), Lagos (36.04%), and Kwara (35.33%) reported the highest food inflation rates, while Sokoto (20.09%), Nasarawa (24.35%), and Jigawa (24.53%) recorded relatively slower increases.

A noteworthy change introduced in July’s report was the exclusion of energy products from the components of core inflation due to the depreciation of the Naira, resulting in higher petroleum product prices. With the deregulation of the oil sector and the removal of subsidies, all items constituting energy are now determined by market forces, leading to price volatility. Consequently, the core inflation segment, now defined as all items excluding farm produce and energy, reached 21.15% in August 2023 on a year-on-year basis. This represents a significant increase of 4.03% points compared to the 17.12% recorded in August 2022. Notably, the highest price increases were observed in passenger transport by air, passenger transport by road, medical services, vehicle spare parts, and maintenance and repair of personal transport equipment.

For urban inflation, the rate surged to 27.69% year-on-year in August 2023 from 20.95% in the corresponding period of 2022. On a monthly basis, the urban inflation rate stood at 3.29%, a 0.24 percentage point increase from the 3.05% reported in July. Rural inflation, on the other hand, reached 24.10% year-on-year, marking a notable 398 basis points increase from the 20.12% observed in the same month of the previous year. The rate for rural inflation also increased by 0.34 percentage points, reaching 3.08% in August from 2.74% in July 2023.

EQUITIES MARKET: Weak Market Momentum Drags the ASI by 0.11% w/w Due to Sell-offs….

The local equities market closed negative on Friday with an 11bps week on week deceleration in the benchmark index to 67,324.59 points, exhibiting weak momentum as investors cherrypicked on highly priced, low, and medium-cap companies despite the postponement of the Central Bank of Nigeria’s upcoming policy meeting and assumption of office by the new acting CBN Governor, and the quarter-end window dressing by fund managers. In tandem with the ASI, the total market capitalization of listed equities experienced a decline of 0.11% week-on-week, descending to N36.85 trillion as the year-todate return of the All-Share Index (ASI) printed at 31.36%.

Turning our attention to sectoral performance, the week unveiled a largely positive outing. The Insurance sector emerged as the top gainer this week by 3.34% week on week and was trailed by the Consumer goods (+2.98%), Banking (+0.61%) and the Oil & Gas sectors (+0.56%) accordingly. On the contrary, the Industrial Goods sector closed the week negative by 4.80% week on week owing price decrease in Dangcem.

Trading activity throughout the week remained characterized by mixed sentiments, as evidenced by the weekly tally of deals which decelerated by 13.70% week-on-week to 38,536 deals. Moreover, the average traded volume witnessed a modest weekly increase of 33.36%, settling at 3.91 billion units. However, the weekly average value declined by 35.97% week on week, and reaching a value of N30.38 billion.

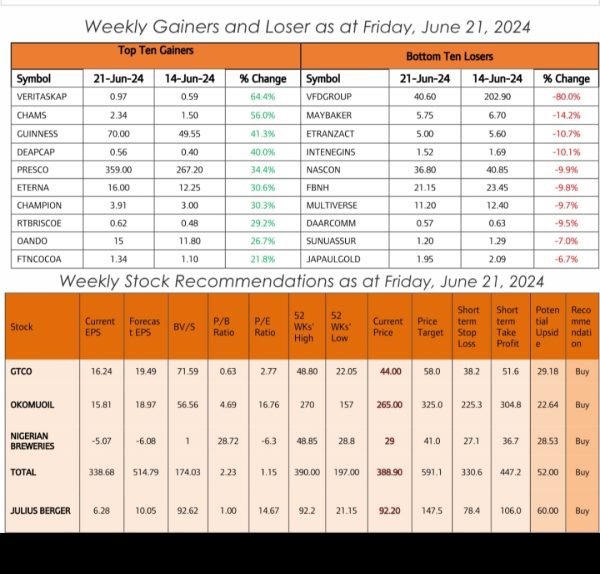

At the close of the week, ELLAHLAKES, E-TRANZACT, CHAMS and JAPAULGOLD were the major toast of investors amid the cherry-picking activities as their share prices advanced by +29%, +29%, +19% and +18% respectively while the laggards for the week were MCNICHOLS, UNITY, DANGCEM whose prices nosedived by -13%, -11% and -8% week on week.

In the upcoming week, we anticipate a blend of mixed sentiments in the market, with positive momentum counterbalanced by profit-taking activities as we approach another potential peak or a possible fake out. This uncertainty is further fueled by the upcoming half-year earnings reports from AccessCorp while investors are likely to continue in portfolio reshuffling in preparation for the quarter-end reporting season. Meanwhile, we continue to advise investors on taking positions in stocks with sound fundamentals.

FOREX MARKET: Speculative Activities Drive Naira to a Historic Low of N998/$1; CBN Sells FX to Banks …..

In the foreign exchange market this week, the naira continues to face significant depreciation pressures against the US dollar at the open market, with forecasts suggesting it may surpass the milestone of N1000 against the dollar in the foreign exchange market before the close of September. This alarming trend is primarily driven by a combination of factors such as dwindling foreign reserves, increased demand for foreign currency, and economic challenges.

This week, the naira gained strength by 1.21% week-on-week at the official market, closing at N747.76/$1 as the CBN supplied forex to deposit money banks and the market to further shore up the value of the naira as part of the interventions by the apex bank. Meanwhile, at the parallel market, the naira depreciated by 4.50% week-on-week to a historic low of N998/$1. This depreciation was driven by the continued search for the dollar by forex users in alternative forex markets, given the limited supply from the apex bank.

Meanwhile, at the FMDQ Securities Exchange (SE) FX Futures Contract Market, the naira gained across board against the US dollar. Notably, forward rates appreciated in favour of the Nigerian legal tender by 1.98%, 2.43%, 2.86%, 4.20%, and 5.49% for the 1-month, 2- month, 3-month, 6-month, and 12-month contract tenors, respectively. This upward movement in forward rates was a result of increased demand for the dollar across these various tenors.

Shifting our focus to the oil market, Oil prices were poised for a marginal weekly decline as markets reacted to the Federal Reserve’s indication that it might maintain higher interest rates for an extended period, despite refraining from a rate hike at its latest meeting. As a response, crude oil prices experienced a weekly increase, with WTI crude trading at around the $90 band per barrel and Brent crude at $93.50 per barrel on Friday. Additionally, the price of Nigerian Bonny Light crude oil closed positively at above $100 to $100.09 per barrel, up from the previous week’s $96 per barrel.

In the coming week, Cowry Research anticipate the naira to trade in a relatively positive band to show further appreciation at the various fx markets barring any distortions while the apex bank maintains its interventions to shore up the naira value.

MONEY MARKET: Money Market Rates Crash on Ease in Financial System Liquidity…

In the just concluded week, we saw yields in the secondary market trended lower for most maturities tracked except for the 6-months maturities whose yield advanced 25bps to 7.82%. Notably, NITTY for 1 month, 3 months, and 12 months maturities crashed to 3.44% (from 3.86%), 5.00% (from 5.08%), and 14.00% (from 14.50%) respectively.

In the same vein, we saw the weekly NIBOR moved in southward direction as the NITTY, with the Overnight NIBOR, the 1- month, and 3-months maturities easing by 22217bps, 79bps and 71bps to 3.00% (from 25.17%), 9.38% (from 10.17) and 9.96% (from 10.67%), respectively, while NIBOR for 6 months tenor bucket recorded an uptick to 11.06% (from 11.00%), respectively.

In the new week, we expect activity in the money market to be bearish as we expect the CBN to rollover a total N177.12 billion maturing treasury bills across the 91-day, 182-day and 364-day tenors at the next primary market auction….

BOND MARKET: Positive Weekly Outing for the FGN Eurobonds…

This week, the values of FGN bonds traded at the secondary market stayed relatively flat across maturities except for the APR-37 which saw sell-off pushed yields higher by 20bps week-on-week while the value tanked to N104.45. Specifically, the MAR 2027, the MAR 2035, and the MAR 2050 debt instruments saw theor their corresponding yields muted at 13.62%, 14.92%, 15.42%, and 15.83% respectively.

Meanwhile, the value of FGN Eurobonds traded on the international capital market appreciated for all maturities tracked, fueled by strong buy sentiment. Notably, the NOV 2027, the FEB 2038, and the NOV 2047 bonds experienced appreciation in value worth USD1.13, USD 0.71, and USD 0.86, respectively, leading to yields contractions to 10.85%, 11.67%, and 11.41%.

In the new week, we expect local OTC bond prices to trade muted as the market seek for trigger for the bullish sentiment in the midst of an expected strain in financial system liquidity…