ECONOMY: Local Investors Flex Investment Muscles Amidst 63% m/m Downturn in Trading Activities on NGX…

Negative sentiment in the local bourse has arisen due to economic uncertainties, including currency fluctuations and inflation, while government policies have introduced an element of unpredictability. Despite these challenges, foreign investors appear to be reevaluating the Nigerian market’s potential, emphasizing the need for a nuanced understanding of the factors influencing market dynamics. Meanwhile, the recent surge in foreign investor activity in the Nigerian stock market stands in contrast to the pre-COVID-19 era when their market share was below 25%. This shift can be attributed to a change in sentiment driven by macroeconomic factors and government policy reforms.

EQUITIES MARKET: Bearish Sentiment Holds Grip by 1.40% w/w on Persistent Sell-Pressure….

In the upcoming week, we anticipate the bearish sentiment to continue as the market seek catalyst and policy pronouncements to trigger the bullish sentiment. However, as we drive into the final quarter for the year and the reporting season draws closer, investors will begin to rebalance their portfolio in their search for alpha in preparation for the quarterending reporting season.

FOREX MARKET: Naira Weakens Further Across Markets as New CBN Chief Takes Office…

In the coming week, Cowry Research anticipate the naira to trade in a relatively calm band barring any further market distortion and as the new CBN chief assumes duty while the market await policy directions and roadmap to ensuring stability of the local currency.

MONEY MARKET: Ease in System Liquidity Spook Money Market Rates ..

In the new week, we expect yields in the secondary market to stay muted as the liquidity inflow and the recent primary market auctions for the treasury bills take significant effects in the market. Thus, yields is expected to remain subdued in the short term.

BOND MARKET: Yields on FGN Securities Push Higher on Sell Pressure…

In the new week, we expect local OTC bond prices to trade muted as the market seek for trigger for the bullish sentiment in the midst of an expected strain in financial system liquidity…

BOND MARKET: Yields on FGN Securities Push Higher on Sell Pressure…

In the new week, we expect local OTC bond prices to trade muted as the market seek for trigger for the bullish sentiment in the midst of an expected strain in financial system liquidity…

This week, we take a cursory look into the activities of portfolio investors through equities on the Nigerian stock exchanges. The data polled from the NGX on domestic and foreign portfolio trading in the month of August 2023 showed that the market witnessed a striking downturn in total trading activity, with figures plummeting by a staggering 62.65% to N262.56 billion, down from July’s robust N702.98 billion. This abrupt dip in market performance raised eyebrows across the financial sector.

Comparing August 2023 to the same month in the previous year, however, a remarkable surge of 111.79% was recorded as the total transaction value in August 2023 stood tall at N262.56 billion, in stark contrast to the more modest N123.97 billion seen in August 2022. Notably, domestic investors flexed their muscles in August 2023, commanding a significant lead over their foreign counterparts, dominating the market by a substantial 72%.

Delving further into the monthly data, it became apparent that domestic transactions bore the brunt of the downturn, plummeting by 65.97% from July 2023’s robust N662.44 billion to N225.40 billion in August 2023. This could be attributed to the effect of the foreign exchange harmonization by the central bank which saw a translation of the exchange rate above N700 from the previous band which was between N435 and N467 per dollar. In parallel, foreign transactions saw a more moderate decline of 8.34%, settling at N37.16 billion in August, compared to N40.54 billion in July 2023.

A closer examination of investor types revealed that institutional investors outpaced retail investors by a notable 14% margin. In particular, retail transactions dwindled by 57.76%, sliding from N229.95 billion in July to N97.13 billion in August 2023. Meanwhile, institutional investments also contracted, albeit by a greater extent, plunging by 70.34% from N432.49 billion in July 2023 to N128.27 billion in August 2023.

Zooming out to a broader perspective, a long-term view spanning sixteen years painted a picture of decline in both domestic and foreign transactions. Domestic transactions witnessed a notable 45.30% decrease from N3.556 trillion in 2007 to N1.945 trillion in 2022. In the same way, foreign transactions displayed a downward trend, declining by 38.47% from N616 billion to N379 billion over the same period. Oddly, domestic transactions dominated the market in 2022, accounting for approximately 84% of the total transactions, leaving foreign transactions with a mere 16% share. Current data for 2023 suggests that total domestic transactions hover around N2.194 trillion, whereas total foreign transactions stand at roughly N222.78 billion.

Negative sentiment in the local bourse has arisen due to economic uncertainties, including currency fluctuations and inflation, while government policies have introduced an element of unpredictability. Despite these challenges, foreign investors appear to be reevaluating the Nigerian market’s potential, emphasizing the need for a nuanced understanding of the factors influencing market dynamics. Meanwhile, the recent surge in foreign investor activity in the Nigerian stock market stands in contrast to the pre-COVID-19 era when their market share was below 25%. This shift can be attributed to a change in sentiment driven by macroeconomic factors and government policy reforms.

EQUITIES MARKET: Bearish Sentiment Holds Grip by 1.40% w/w on Persistent Sell-Pressure….

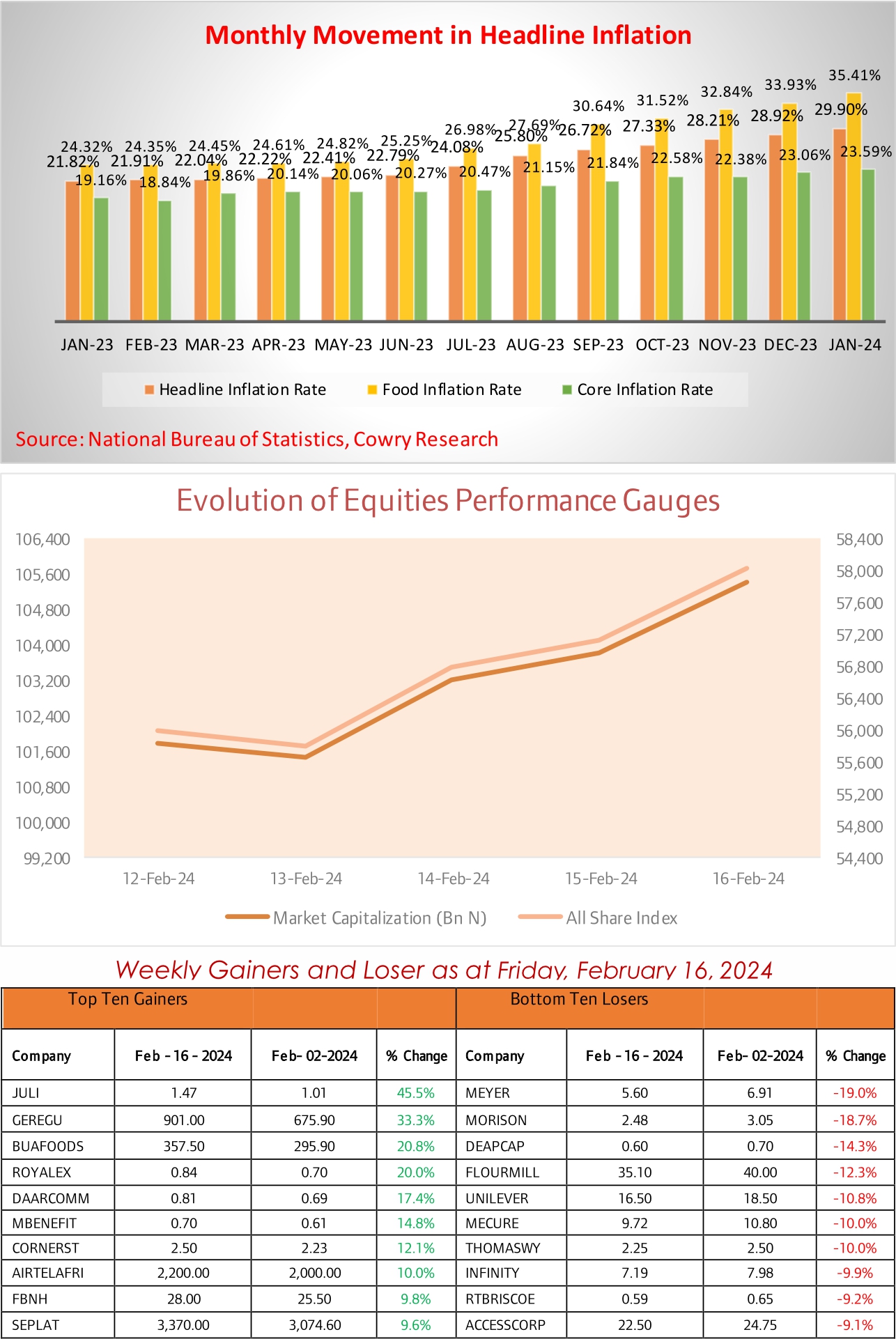

It was another negative outing this week for the local equities market as the All-Share Index declined by 1.40% week on week to 66,382.14 points just as sell-off activities and profit-taking in the some of the blue-chip companies continues. In tandem with the ASI, the total market capitalization of listed equities experienced a decline of 1.40% week-on-week, descending to N36.33 trillion as the year-to-date return of the All-Share Index (ASI) eased to 29.52%.

The sectoral performance was in the mix-bargain as the see-saw movement continues across tickers. The Insurance and consumer goods sectors were the best performing indices as they garnered gains by 2.77% and 1.59% week on week. On the flip side, the Banking (-4.17%), the Industrial goods (-3.04%) and the Oil & Gas sectors (-1.24%) accordingly posted weekly losses as investors dump securities across these indices.

Trading activity throughout the week remained characterized by waning sentiments, as evidenced by the weekly tally of deals which decelerated by 27.67% week-on-week to 27,874 deals. Moreover, the average traded volume witnessed a weekly decrease by 65.76%, settling at 1.34 billion units while the weekly average value declined by 41.03% week on week, and reaching a value of N17.92 billion.

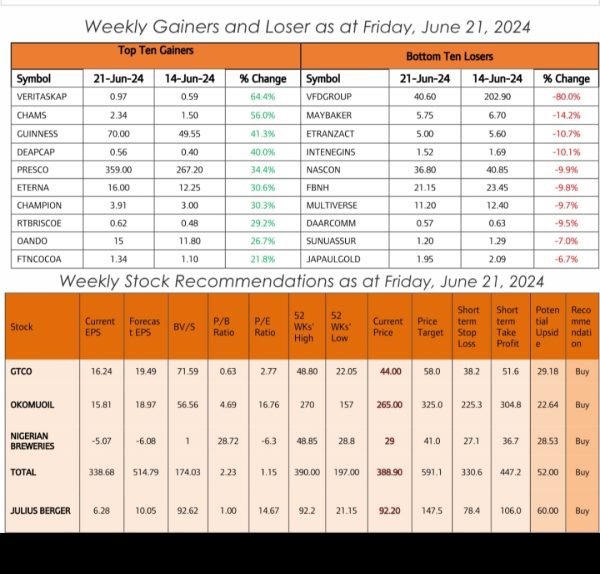

At the close of the week, SUNUASSURE, DAARCOMS and ETERNA were the major toast of investors amid the cherry-picking activities as their share prices advanced by +19%, +19%, and +15% respectively while the laggards for the week were OANDO, TANTALIZER, and CHAMS whose prices nosedived by -19%, -14% and -10% week on week.

In the upcoming week, we anticipate the bearish sentiment to continue as the market seek catalyst and policy pronouncements to trigger the bullish sentiment. However, as we drive into the final quarter for the year and the reporting season draws closer, investors will begin to rebalance their portfolio in their search for alpha in preparation for the quarter-ending reporting season. Meanwhile, we continue to advise investors on taking positions in stocks with sound fundamentals.

FOREX MARKET: Naira Weakens Further Across Markets as New CBN Chief Takes Office…..

This week, the naira grappled with strength against the dollar at the various fx segments despite the confirmation of the new CBN Governor, its Board members and the identification of policy directions of the new CBN leadership. Thus, the naira lost strength by 1.00% week-on-week at the official market, closing at N755.27/$1. Meanwhile, at the parallel market, the naira depreciated by 1.00% week-on-week to a historic low N1,008/$1 as demand pressure continues from fx users.

Meanwhile, at the FMDQ Securities Exchange (SE) FX Futures Contract Market, the dollar gained across board against the local currency. Notably, forward rates appreciated in favour of the dollar by 1.17%, 1.10%, 0.97%, 0.73%, and 1.03% for the 1-month, 2-month, 3-month, 6-month, and 12-month contract tenors, respectively. This upward movement in forward rates was a result of increased demand for the dollar across these various tenors.

Shifting our focus to the oil market, WTI crude oil futures rose to $90.7 per barrel on Tuesday, marking their highest level since November on the back of expectations of larger market deficits in the fourth quarter, offsetting concerns regarding a potential economic recession’s impact on oil demand. Additionally, the price of Nigerian Bonny Light crude oil closed positively at $100.69 per barrel on the back of strong demand.

In the coming week, Cowry Research anticipate the naira to trade in a relatively calm band barring any further market distortion and as the new CBN chief assumes duty while the market await policy directions and roadmap to ensuring stability of the local currency.

In the just concluded week, we saw yields in the secondary market trended lower for most maturities tracked following the renewed interest seen at the recent auction. Notably, NITTY for 1 month, 3 months, 6- months and 12 months maturities crashed to 3.38% (from 3.44%), 4.44% (from 5.00%), and 13.94% (from 14.04%) respectively. Also, the weekly NIBOR moved southward on the back of ease in the financial system liquidity which was spurred by over N1 trillion FAAC inflow. Consequently, the Overnight NIBOR stayed flat from the prior week at 3.00%, while the 1-month, and 3-months maturities NIBOR retreated by 1.88% points, 1.29% points and 1.39% points to 7.50% (from 9.38%), 8.67% (from 9.96%) and 9.67% (from 11.06%), respectively. On Thursday, the Central Bank of Nigeria (CBN) conducted its Primary Market auction for Nigerian treasury bills, successfully selling maturing bills with a total value of N177.12 billion. These bills were offered across three different tenors: N1.75 billion for the 91-day maturity, N1.56 billion for the 182-day maturity, and the bulk of N173.81 billion for the 364-day maturity. The outcome of the auction points to robust investor appetite for Nigerian treasury bills, with increased subscription levels and declining stop rates.

The auction attracted a total subscription of N786.79 billion, a significant increase from the N643.89 billion recorded at the previous auction. This surge in subscription led to a bid-to-cover ratio of 4.44x across all maturity periods, compared to the 4.23x ratio observed in the previous auction. One noteworthy development was the decline in stop rates across all tenors. The rates dropped to 4.99% for the 91-day bills (from 6.50% previously), 6.55% for the 182-day bills (compared to 7.00% previously), and 11.37% for the 364-day bills (down from 12.98% previously) and the majority of the demand was focused on the 364-day bills, indicating a preference among investors for longer-term securities.

In the new week, we expect yields in the secondary market to stay muted as the liquidity inflow and the recent primary market auctions for the treasury bills take significant effects in the market. Thus, yields is expected to remain subdued in the short term.

BOND MARKET: Yields on FGN Securities Push Higher on Sell Pressure…

This week, the values of FGN bonds traded at the secondary market stayed relatively flat across maturities except for the APR-37 which saw sell-off pushed yields higher by 54bps week-on-week. Meanwhile, the MAR 2027, the MAR 2035, and the MAR 2050 debt instruments saw their corresponding yields closing the week at 13.59%, 14.93%, and 15.83% respectively.

Meanwhile, the value of FGN Eurobonds traded on the international capital market closed in the bearish region on the back of rising oil prices, and fueled by mild sell sentiment as they nosedived by 1.21% points, 1.95% points and 1.76%. Notably, the NOV 2027, the FEB 2038, and the NOV 2047 instruments saw their respective yields expanding at the close of the week to 11.97%, 12.39%, and 12.06%.

In the new week, we expect local OTC bond prices to trade muted as the market seek for trigger for the bullish sentiment in the midst of an expected strain in financial system liquidity…