MARKET UPDATE

ECONOMY: Restricted Investible Options Still Drags Pension Industry Amid AuM Growth to N14.59 Trillion

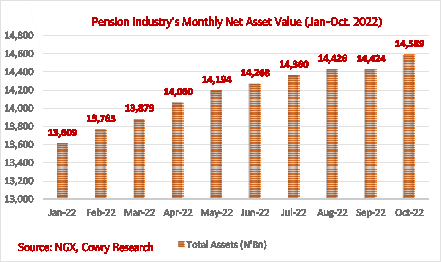

The latest data obtained from the National Pension Commission, the total Pension Industry assets undermanagement have risen further by 8.72 per cent to N14.59 trillion as of October2022 from N14.42 trillion in the prior month (September 2022) and N13.42trillion at the end of the fourth quarter of 2021. This tremendous growth can be attributed to the increase in the level of compliance by the public and private sector employers as a result of the various steps taken by the Commission to improve compliance and coverage as well as enhanced market penetration and strategies deployed by the PFAs. The Nigerian pension industry has transited from being just a governmentfunded scheme to both private and public sector participation. However, statistics have shown that the industry has grown by more than 600 per cent in terms of pension fund assets size which is a clear indication of the industry’s growth and evolution as well as the continued acceptance of the scheme by workers in both the formal and informal sector. So far in 2022, the rise in total industry assets was principally driven by the continued rising exposure of fund managers to securities of the federal government in the face of interest rate hikes by the central bank plus the attractive money market instruments amid rising fixed income yields. Meanwhile, it is pertinent to avow here that Nigeria’s pension sector has grown remarkably since 2004 when the Pension Reform Act was passed, there is still some ground to cover and this can be achieved with continuing investor education and efforts aimed at driving a significant penetration into the space. With a positive rise in the number of contributors to 9.85 million members at the end of October, the total number of contributions is expected to surpass the 10 million membership mark by the close of the year with the total pension assets projected to reach N14.8trillion by the end of 2022. For the record, the funds have continued to favour the Nigerian government’s debt securities as an asset class resulting from the scantiness of good quality investible securities available to them. From the report from PenCom, PFA’s investment into FGN Securities has remained the principal driver of the monthly gains as it holds over 60 per cent in FGN Bonds worth N8.84 trillion at the end of October. Also, money market instrument accounts for almost 15 per cent of PFA holdings while corporate debt securities accounted for 10.5 per cent of the total industry holdings in various asset classes. Elsewhere, PFA holdings in domestic shares from the local equities market dwindled further to merely 5.6 per cent which was principally attributed to the lack of depth of the equities market which recorded the worst decline so far this year in the month of October.

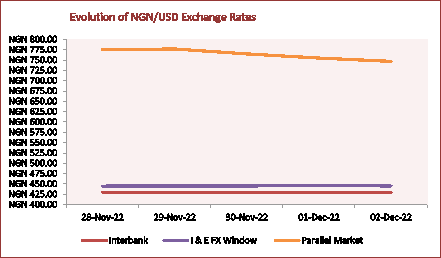

FOREX MARKET: Naira Appreciates Against USD Across FX Markets As New Banknotes Rollout Draws Near… In the just concluded week, we saw the Naira experience another calm in demand in the foreign exchange market as Bureau De Change operators cut rates in a bid to attract users of the greenback just as we inch closer to the official date of the release of the redesigned Naira notes by the CBN. Consequently, at the the open parallel market FX window the Naira strengthened further by N28 or 3.6% week on week to close the week at N747/USD from N775/USD in the previous week’s close as currency users continue to dump the greenback. Similarly, the Naira edged the dollar by N1 (0.22%) week on week at the importers and exporters window to close the week at N445.33 from N446.33/USD the previous week as demand for the greenback took a breather. Thus, market participants maintained bids between N444/USD and N450/USD at the I&E segment while at the open market, bids ranged between N740/USD and N753/USD. A look at activities at the Interbank Foreign Exchange Forward Contracts market, the spot exchange rate remained unchained from the previous week as it closed the week at N445/USD from last week. Also, our analysis of the Naira/USD exchange rate in the Naira FX Forward Contracts Markets, there was a bearish trend across tenors for the Naira Forward Contracts against the greenback as we saw depreciating of the Naira index across all tenors by 1.89%, 2.46%, 2.81%, 3.16% and 4.45% week on week across all tenor gauges to close the week at offer prices of N460.03/USD, N466.18/USD, N471.58/USD, N491.30/USD and N525.75/USD in that order. Elsewhere, the Bonny light crude price dipped by 2bps week on week to close the week at USD87.40 per barrel (as at November 30,) from USD87.42 per barrel in the previous week. This is emanating from the uncertainties around the global crude oil price in the face of latest updates on the covid-19 pressures in two cities of China and a steady US inventories. Just as was witnessed in the last week, we see further appreciation across all FX segments as the date for new banknotes rollouts draws closer and barring any distortion in the market. This appreciation is expected to continue as we head into the festive season despite the high momentum in campaign activities.

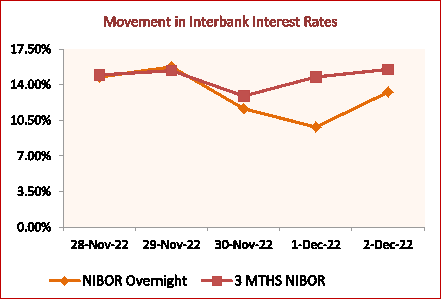

MONEY MARKET: : NITTY Moves Southwards for Most Maturities amid Muted Primary Market Sales… In the just concluded week, activity in the money market was muted given the zero matured and auctioned Treasury bills. This created a buy sentiment in the secondary market as investors rushed to this space to mop up bills. Hence, NITTY fell for most maturities amid sustained bullish pressure. NITTY for 1 month, 3 months, 6 months, and 12 months moderated to 9.17% (from 10.10%), and 8.97% (from 10.19%). 10.32% (from 11.57%) and 14.89% (from 17.08%) respectively. Meanwhile, N25 billion in OMO bills matured without refinancing in the market. Notably, we witnessed tighter liquidity conditions on the back end of the curve as NIBOR closed in a bearish manner for the 3-month and 6-month tenor buckets, rising to 15.50% (from 15.16%) and 16.13% (from 15.86%), respectively, due to the relatively low value of matured OMO bills. The overnight Funds and the 1-Month tenor bucket, on the other hand, fell to 13.25% (from 13.80%) and 14.25% (from 14.60%), respectively. In the new week, we expect activity in the money market to be bearish amid limited maturing Treasury and OMO bills.

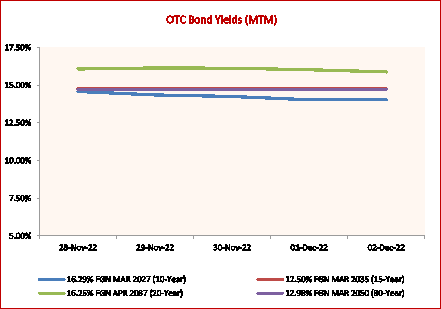

BOND MARKET: FGN Bonds Yields Move in Mixed Directions Across Maturities Tracked… In the just concluded week, the value of FGN bonds moved in mixed directions across maturities tracked. Specifically, the 10-year 16.29% FGN MAR 2027 debt and the 20-year 16.25% FGN APR 2037 bond gained N1.79 and N0.78 respectively; their corresponding yields fell to 14.03% (from 14.58%) and 15.88% (from 16.02%) respectively on demand pressure. However, the 15-year, 12.50% FGN MAR 2035 paper and the 30- year 12.98% FGN MAR 2050 debt remained unchanged as their corresponding yields stayed flat at 14.75% and 14.72% respectively. Elsewhere, the value of FGN Eurobonds traded in the international capital market appreciated for most maturities tracked on buy interest; hence the 20-year, 7.69% paper FEB 23, 2038; and the 30-year, 7.62% NOV 28, 2047, gained USD 0.51, and USD 0.20, respectively, while their corresponding yields fell to 12.00% (from 12.09%), and 11.76% (from 11.80%). Meanwhile, the 10-year, 6.375% JUL 12, 2023, bonds lost USD 0.01 as its corresponding yield rose by 9.06% (from 8.96%). In the new week, we expect the value of FGN Eurobonds to further rise (and yields to decrease) as rates remain attractive at upper band of 9%.

EQUITIES MARKET: Strong Buying Interest in Banking, Oil/Gas, Others Signals Return of Strength with N327bn Gains…

After a bullish and volatile November which saw investors took profits worth N2 trillion amid buying interests, the domestic market benchmark index kickstarted December with a 1.26% week on week surge and crossing the 48,000 psychological mark to 48,154.65 points while the market capitalisation inched higher in the same route by 1.26% week on week to N26.23 trillion signaling an uptrend and a relative return of strength to the market. Although, the upbeat in market perfomance was buoyed by price appreciations and strong buying demands in some of the banking and insurance stocks, investors took profit worth N326.98 billion from 3 of the 5 sessions. Consequently, the positive sentiment and buying pressure was followed by the low price to earnings ratio after market players had done their analysis of the nine-month earnings reporting which supported market fundamentals. And as a result, we saw gains from price appreciation in tickers such as PZ (+15%), UACN (+14%), WEMABANK (+10%), ARDOVA (+10%) and NEM (+9%) respectively. With the upbeat in momentum, the sectorial performance was largely bullish in the week with 3 out of 5 sectors closing northward as the NGX Insurance emerged the leading advancer (+2.23%) for the week and followed by NGX Banking Index and NGX Oil/Gas Index which closed positive by +1.73% and +0.44% from the prior week. On the flip side, the NGX Industrial Goods (-0.94%) and NGX Consumer Goods (-0.29%) sectors closed the week as the losers. Meanwhile, the level of trading activities in the week was varied as the total traded volume surged by 18.04% w/w to 839.97 million units. However, the total weekly traded value dipped by 24.89% week on week to N7.37 billion and then the total deals traded for the week tanked by 2.87% week on week to 16,183 trades for the week. Going into the new week, we expect a bullish momentum as investors begin to rebalance their portfolios as the year begins to wound down with optimism for full-year higher dividends payment. However, we continue to advise investors to trade on companies’ stocks with sound fundamentals and a positive outlook amid the macro-dynamics which remains a headwind.